Corporate Governance Update

SEC Seeks Additional Feedback on Proposed Compensation Clawback Rules

On October 14, 2021, the U.S. Securities and Exchange Commission (SEC) reopened the period to solicit input from the public on the compensation clawback rules it proposed in 2015 to implement Section 954 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). The proposed rules would direct the national securities exchanges to establish listing standards that would require a company to adopt, disclose and comply with a compensation clawback policy as a condition to listing securities on a national securities exchange.

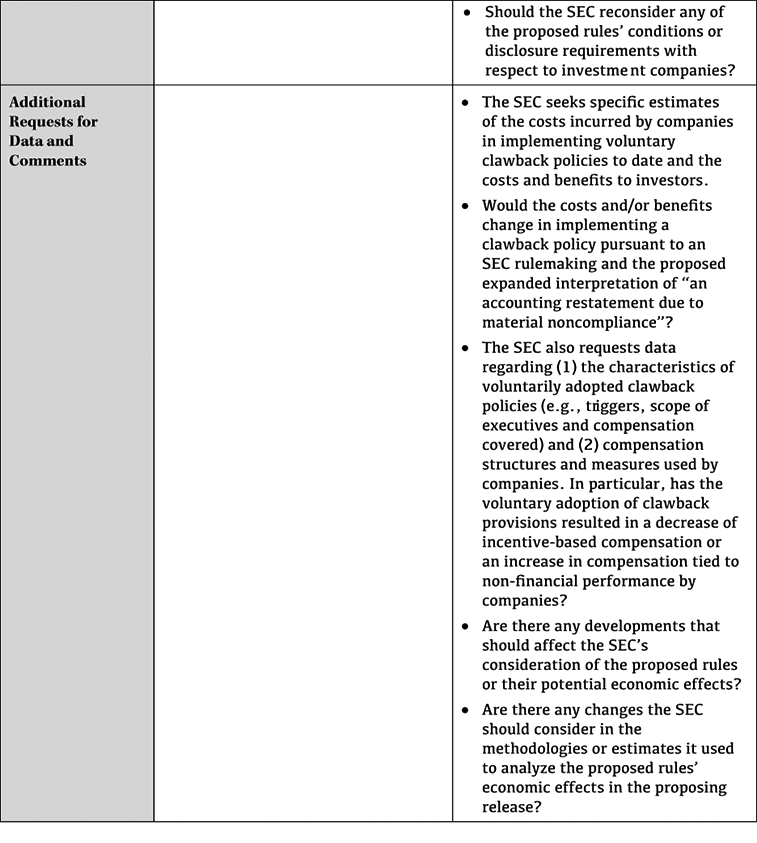

In the reopening release, the SEC requests comments and supporting data on the proposed clawback rules in light of regulatory and market developments since the rules were proposed in 2015. The SEC also identifies 10 new topics on which it is specifically requesting public comment, including the following:

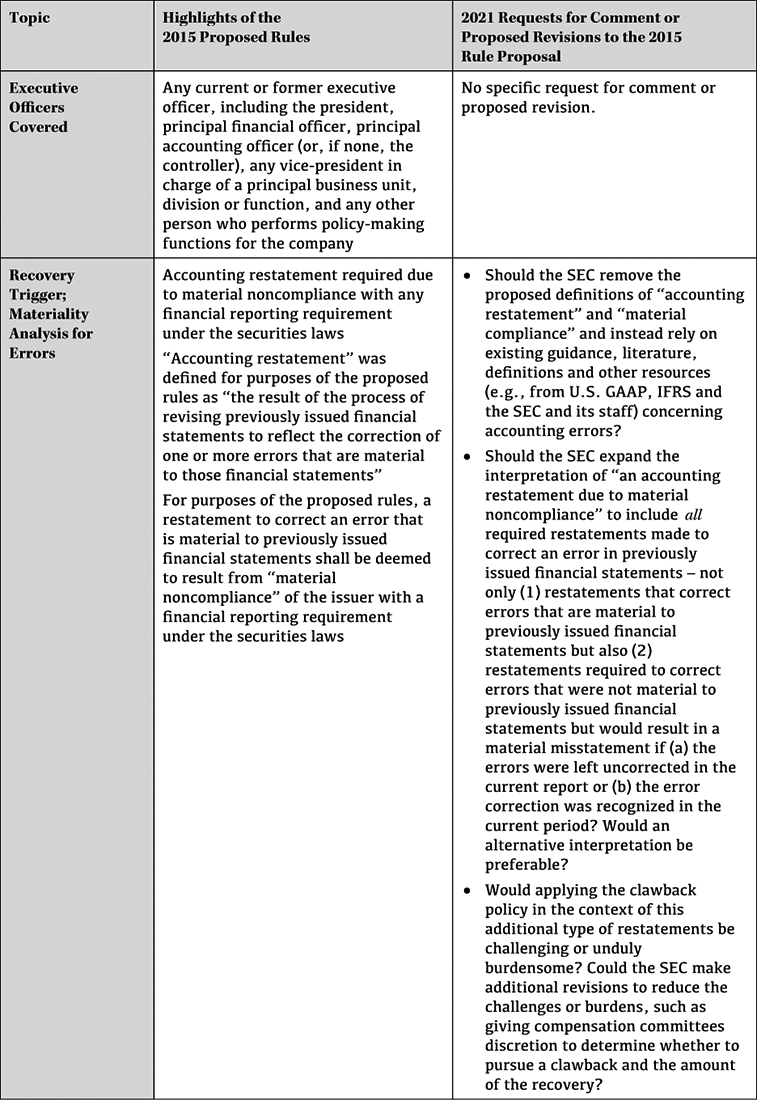

- The SEC asks whether it should expand the types of accounting restatements that would trigger application of a clawback policy. Under Section 954 of the Dodd-Frank Act, a clawback would be triggered “in the event that the issuer is required to prepare an accounting restatement due to the material noncompliance of the issuer with any financial reporting requirement under the securities laws.” Based on its initial interpretation of the Section 954 mandate, the clawback trigger under the SEC’s 2015 proposed rules was limited to material restatements of previously issued financial statements (so-called “Big R restatements”). In the reopening release, the SEC asks the public whether it should expand its interpretation and revise the rule proposal to include all required restatements made to correct an error in previously issued financial statements, including restatements required to correct errors that were not material to previously issued financial statements but would result in a material misstatement if (1) the errors were left uncorrected in the current report or (2) the error correction was recognized in the current period (so-called “Little R restatements”). This new request resulted from concerns raised that companies may not be making appropriate materiality determinations for errors to avoid triggering application of a clawback policy.

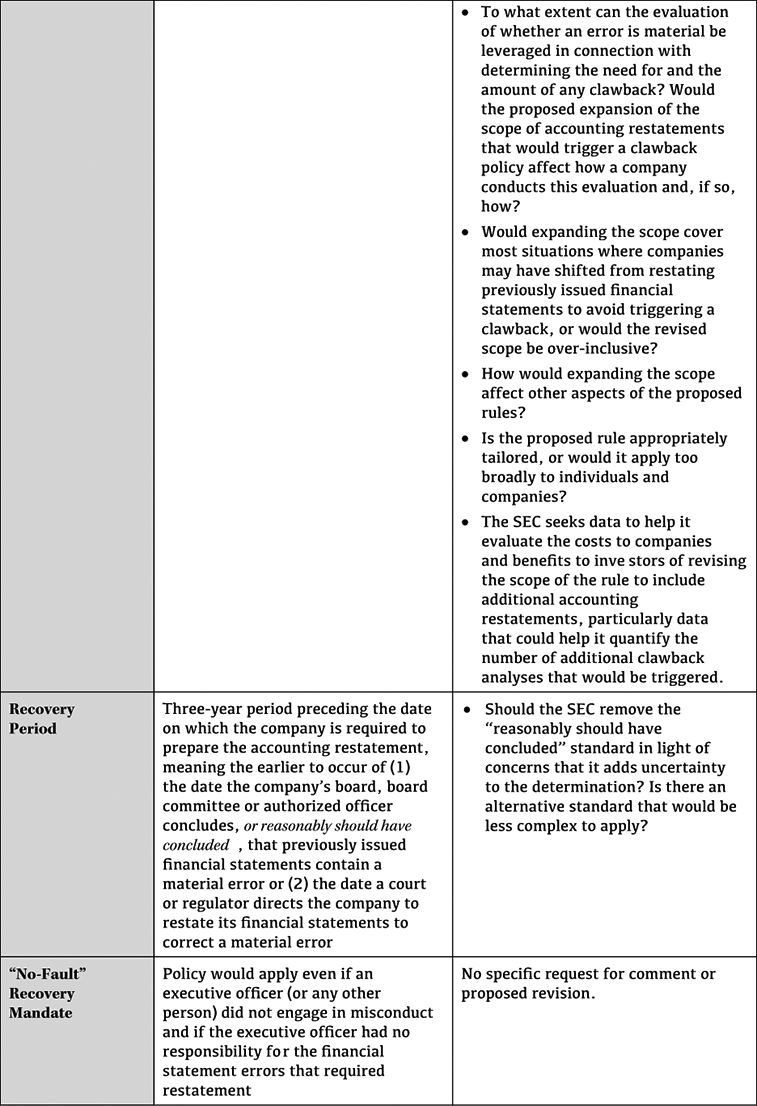

- The proposed rules contemplate that clawback policies would require the recoupment of excess incentive-based compensation received during the three-year period preceding “the date on which the issuer is required to prepare an accounting restatement,” meaning the earlier to occur of (1) the date the company’s board of directors, a board committee or authorized officer (if board action is not required) concludes, or reasonably should have concluded, that the company’s previously issued financial statements contain a material error or (2) the date a court or regulator directs the company to restate its previously issued financial statements to correct a material error. In the reopening release, the SEC asks whether it should remove the “reasonably should have concluded” standard in light of concerns that it adds uncertainty to the determination.

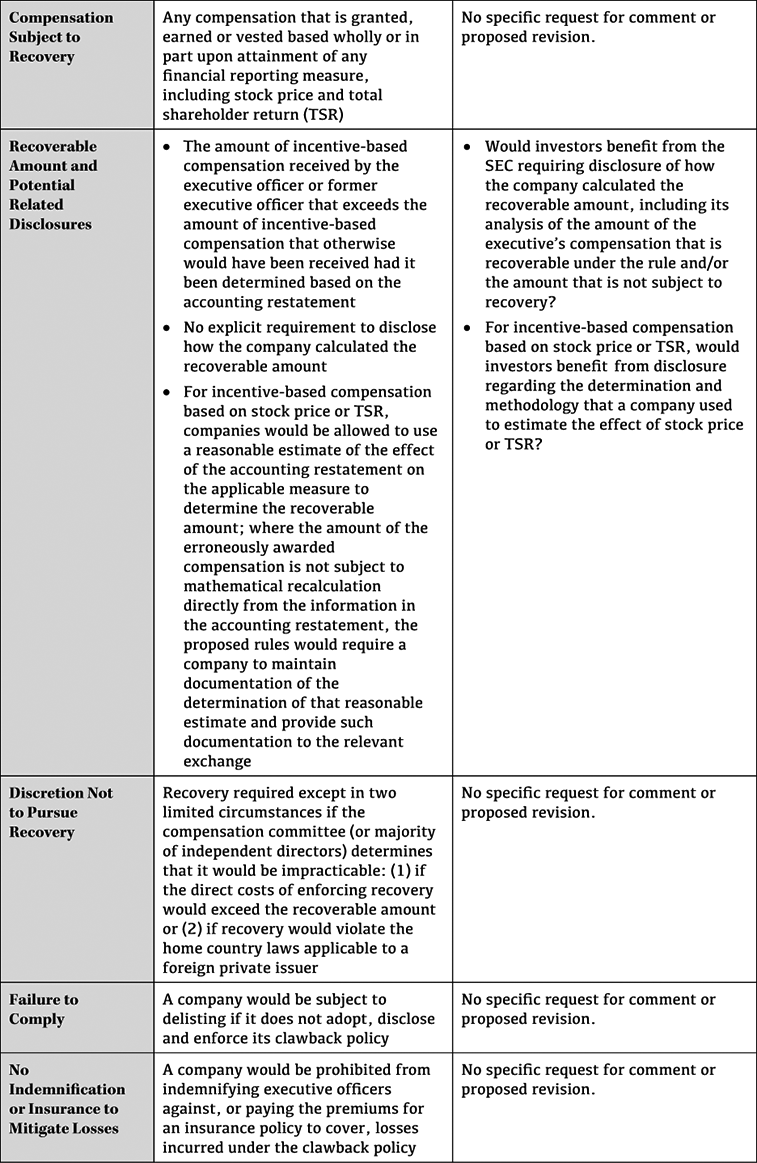

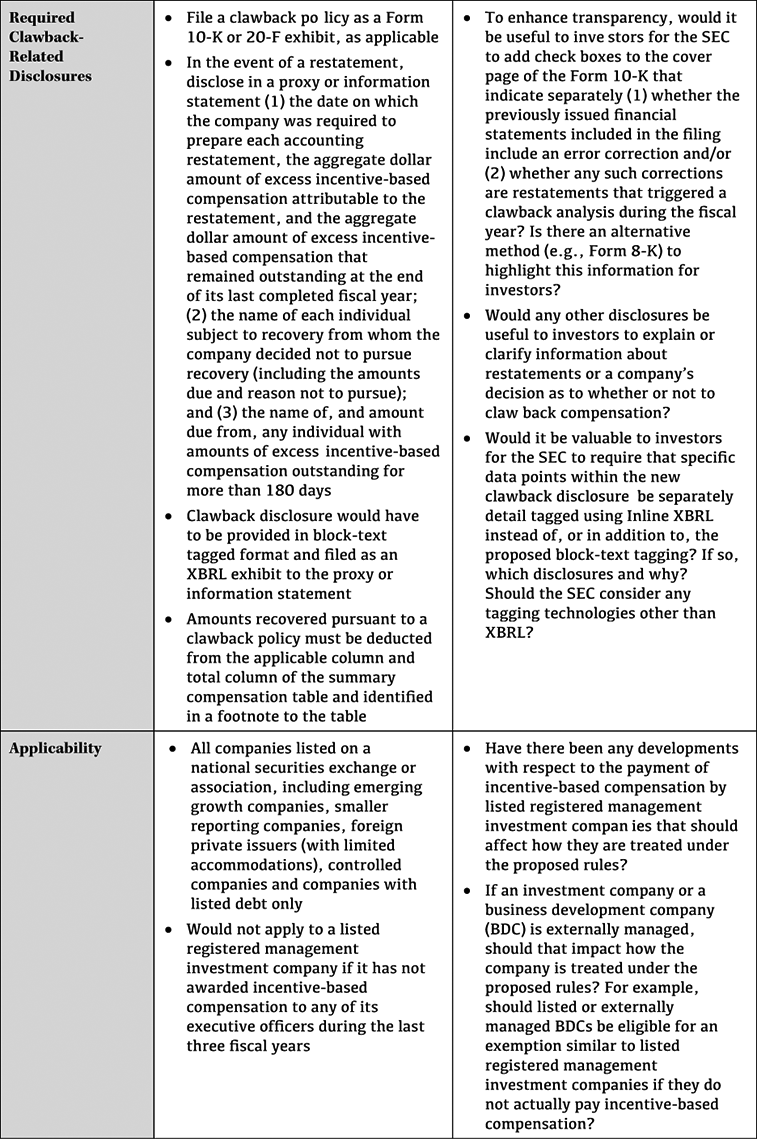

The chart below summarizes the highlights of the clawback rules proposed in 2015 and, where applicable, corresponding requests for comment and proposed revisions to the rule proposal the SEC raised in the reopening release. The comment period will end 30 days after the reopening release is published in the Federal Register.

Practical Implications

In light of the reopening release, companies may consider submitting or contributing to a comment letter on the proposed clawback rules or the specific requests for comment to the SEC. Interested parties may submit comments here, and comments received to date are available here.

We do not know whether the proposed rules will be adopted and, if so, when the corresponding listing standards will be proposed and become effective. It is also uncertain what the terms of the listing standards will be and whether there will be meaningful differences in the standards adopted by the major securities exchanges. In the meantime, companies may consider refreshing their compensation committees on the proposed rules and their implications and reviewing their current clawback policies for consistency with the proposed rules and analyzing what revisions would be necessary.

弁護士広告—Sidley Austin LLP はグローバルな法律事務所です。当事務所の所在地および連絡先情報は、www.sidley.com/en/locations/offices に掲載されています。

Sidley は、本情報をクライアントおよび関係者の皆様へのサービスとして、教育目的のみに提供しています。本情報は、法的助言として解釈または依拠されるべきものではなく、また弁護士と依頼者の関係を生じさせるものでもありません。読者は、専門家の助言を求めることなく本情報に基づいて行動すべきではありません。Sidley および Sidley Austin とは、www.sidley.com/disclaimer に記載のとおり、Sidley Austin LLP およびその関連パートナーシップを指します。

© Sidley Austin LLP

お問い合わせ

この Sidley Update に関してご質問がある場合は、通常ご担当されている Sidley の弁護士、またはご連絡ください。

得意分野

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory