Corporate Governance Update

SEC Proposes to Update Disclosures about Business Description, Legal Proceedings and Risk Factors Required by Regulation S-K

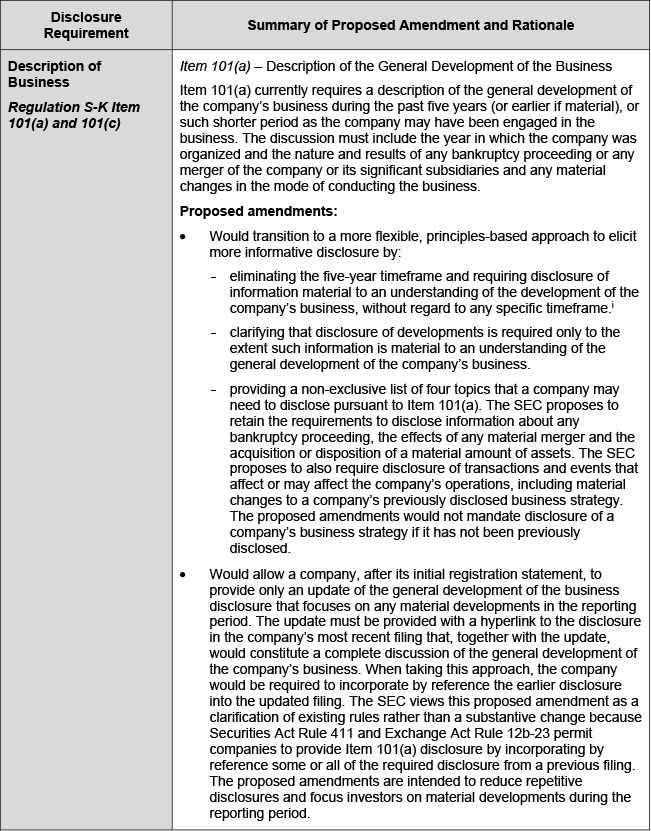

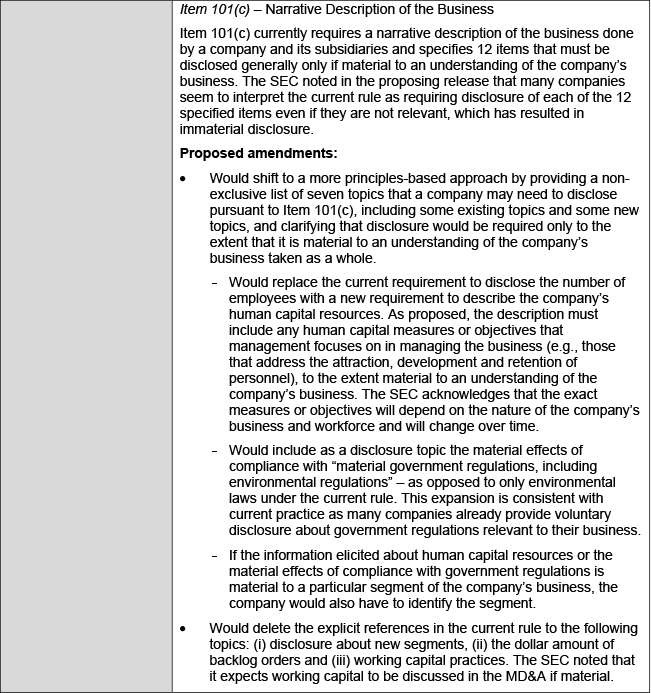

On August 8, 2019, the Securities and Exchange Commission (SEC) proposed amendments to modernize its rules requiring disclosure about a company’s business description, legal proceedings and risk factors. Proposed amendments to Items 101, 103 and 105 of Regulation S-K would:

- give a company more flexibility to tailor the description of its business to its particular circumstances;

- reduce disclosure about matters that are not material to an understanding of a company’s business or legal proceedings; and

- encourage risk factor disclosure that is streamlined, well-organized and limited to material risks.

The proposed amendments are part of the ongoing Disclosure Effectiveness Initiative led by the SEC’s Division of Corporation Finance (Corp Fin) to review and improve the effectiveness of its disclosure requirements for the benefit of investors and companies. It has been more than 30 years since the SEC has significantly revised Items 101, 103 and 105 of Regulation S-K. The proposed amendments are intended to enhance the readability of disclosures, discourage repetitive and immaterial disclosures and reduce the compliance burden on companies. The proposed amendments were informed by input from public comment letters and Corp Fin’s disclosure review process. They are also responsive to changes in the regulatory, business and technological environment since the adoption of Regulation S-K and increasing calls for the SEC to require human capital disclosure.

The proposed amendments are summarized in the table below. The SEC will accept public comments on the proposal for 60 days following its publication in the Federal Register.

1 The SEC similarly proposes to eliminate the timeframe prescribed in Item 101(h), which currently requires smaller reporting companies to describe the development of their business during the past three years.

Attorney Advertising—Sidley Austin LLP is a global law firm. Our addresses and contact information can be found at www.sidley.com/en/locations/offices.

Sidley provides this information as a service to clients and other friends for educational purposes only. It should not be construed or relied on as legal advice or to create a lawyer-client relationship. Readers should not act upon this information without seeking advice from professional advisers. Sidley and Sidley Austin refer to Sidley Austin LLP and affiliated partnerships as explained at www.sidley.com/disclaimer.

© Sidley Austin LLP

Contacts

If you have any questions regarding this Sidley Update, please contact the Sidley lawyer with whom you usually work, or

Capabilities

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory