Corporate Governance Update

SEC Proposes to Update Disclosures about Business Description, Legal Proceedings and Risk Factors Required by Regulation S-K

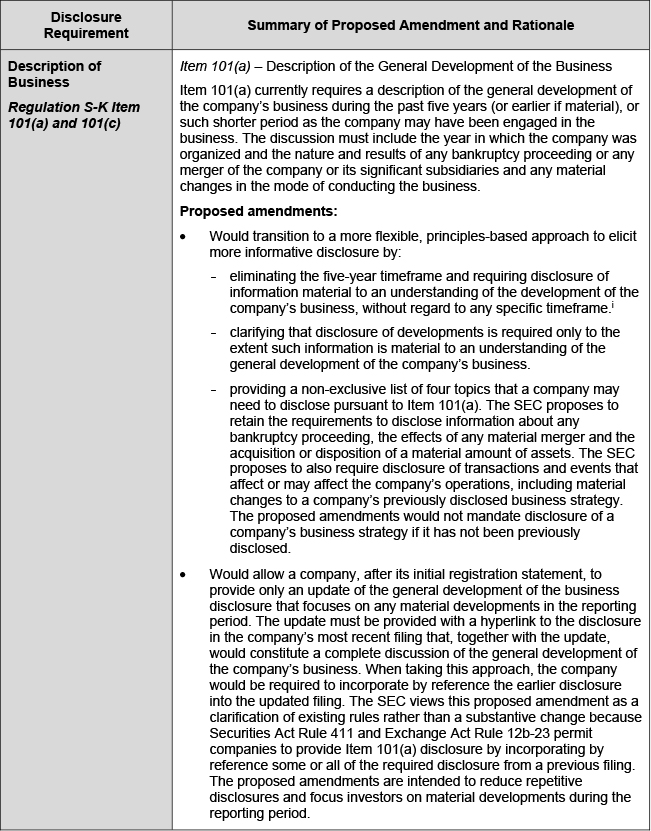

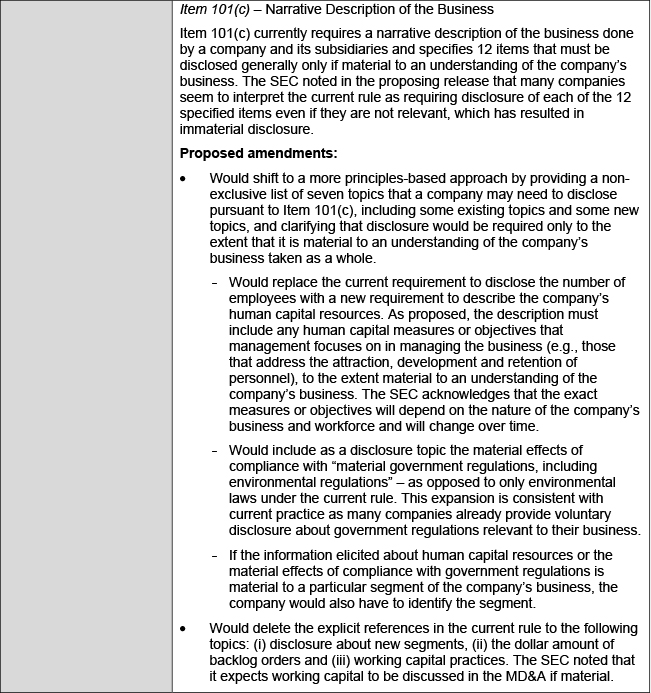

On August 8, 2019, the Securities and Exchange Commission (SEC) proposed amendments to modernize its rules requiring disclosure about a company’s business description, legal proceedings and risk factors. Proposed amendments to Items 101, 103 and 105 of Regulation S-K would:

- give a company more flexibility to tailor the description of its business to its particular circumstances;

- reduce disclosure about matters that are not material to an understanding of a company’s business or legal proceedings; and

- encourage risk factor disclosure that is streamlined, well-organized and limited to material risks.

The proposed amendments are part of the ongoing Disclosure Effectiveness Initiative led by the SEC’s Division of Corporation Finance (Corp Fin) to review and improve the effectiveness of its disclosure requirements for the benefit of investors and companies. It has been more than 30 years since the SEC has significantly revised Items 101, 103 and 105 of Regulation S-K. The proposed amendments are intended to enhance the readability of disclosures, discourage repetitive and immaterial disclosures and reduce the compliance burden on companies. The proposed amendments were informed by input from public comment letters and Corp Fin’s disclosure review process. They are also responsive to changes in the regulatory, business and technological environment since the adoption of Regulation S-K and increasing calls for the SEC to require human capital disclosure.

The proposed amendments are summarized in the table below. The SEC will accept public comments on the proposal for 60 days following its publication in the Federal Register.

1 The SEC similarly proposes to eliminate the timeframe prescribed in Item 101(h), which currently requires smaller reporting companies to describe the development of their business during the past three years.

律师广告—Sidley Austin LLP 是一家全球性律师事务所。我们的地址及联系方式可在 www.sidley.com/en/locations/offices 查阅。

Sidley 提供本信息仅作为向客户及其他友好人士提供的服务,且仅供教育目的使用。本信息不应被解释或依赖为法律意见,亦不构成律师与客户关系。读者在未寻求专业顾问意见之前,不应依据本信息采取任何行动。Sidley 和 Sidley Austin 指 Sidley Austin LLP 及其关联合伙实体,详见 www.sidley.com/disclaimer。

© Sidley Austin LLP

联系我们

如果您对本次 Sidley 更新有任何疑问,请联系您平时合作的 Sidley 律师,或

Capabilities

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory